When Money Earns Nothing: Japan's 30 Year Money Lesson

Think about a stock market that goes nowhere for thirty years. Now think about a bank that pays you almost no interest on your savings. For most people this…

Think about a stock market that goes nowhere for thirty years. Now think about a bank that pays you almost no interest on your savings. For most people this sounds impossible. But this was real life in Japan from the early 1990s until just two years back. It is the best example we have of what happens when a country gets stuck with low growth, falling prices and very low interest rates. And it shows what all this does to normal people and their money. So this is a before and after story.

A market that forgot how to go up

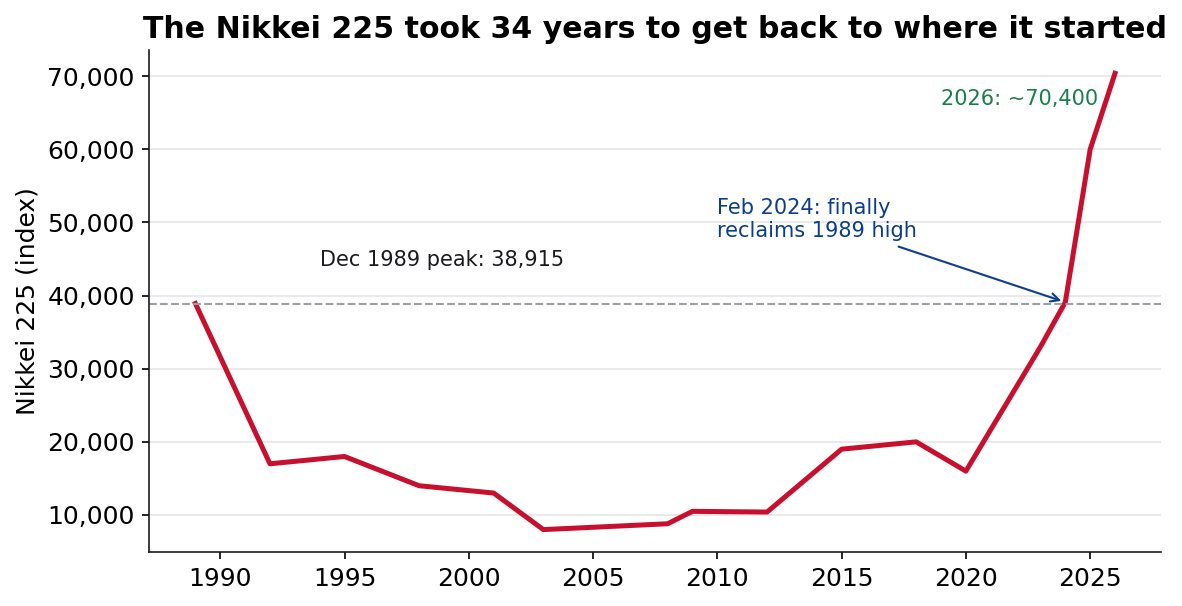

In December 1989 the Nikkei, which is Japan's main stock market, touched 38,915. It was the top of a giant bubble. Land in Tokyo was so costly on paper.

Then the bubble popped. And it did not just fall a little and bounce back. It stayed down for a full generation.

The market did not come back to that 1989 level until February 2024. That is 34 years. A person could join a job, work a full life, and retire without ever seeing the market reach where it started. Even prices of normal things kept same or falling year after year. We call this deflation. It sounds nice if you are a buyer, but it is actually bad. If a TV will be cheaper next month, you wait. Everybody waits. So shops sell less, companies earn less, and the whole economy slows down and gets stuck.

Banks that paid you nothing

To fight this problem, the Bank of Japan pushed interest rates down to zero. Later it even went below zero.

For a normal saver this was slow torture. For years a simple bank account gave around 0.001 percent a year. Keep ten lakh yen in the bank and you might get ten yen back. That is not enough even for a can of coffee. So money kept in the bank just did not grow at all.

So picture the life of a Japanese saver for thirty years. The stock market only seemed to go down. The bank gave nothing. Both doors were closed. So what did people do? They just sat on cash.

This is the biggest point of the whole story. Even today, Japanese families keep about 49 percent of their money in cash and bank deposits. American families keep only about 8 percent. Thirty years of a flat market taught a whole country one belief. Shares lose money, cash is safe. This belief went so deep that even when the rest of the world was making big money in shares, Japanese people stayed in cash and earned nothing. And for a long time it made sense. If prices are flat, then cash that earns nothing still buys the same things. So you lose nothing.

The good side people forget

It is easy to call this a thirty year failure. But it was not fully bad. When such a big bubble breaks, normally you see many companies shutting down and huge job losses, like the 1930s. Japan avoided all that. For thirty slow years, very few people lost their jobs and life stayed calm and safe. The very low rates also let the government carry a huge loan, more than 250 percent of the country's yearly income, at almost no cost. And because Japan tried zero rates and money printing first.

The after part: why things changed

Then three things happened together. Prices started rising again after the pandemic and the 2022 oil shock. So now cash sitting at zero was losing value every year. The Bank of Japan ended its below zero rate in March 2024, and by June 2026 it raised the rate to 1 percent. And the stock market finally woke up, with the Nikkei going past its old top to around 70,000.

Going back to normal rates is actually good for Japan. Savers finally earn something on their big pile of cash, and this helps old people the most. Rising rates also tell people that the falling price problem is over, so they spend now instead of waiting. Banks become healthy again because they earn a proper gap between deposit rate and loan rate. And the central bank gets back its power to cut rates later if a bad time comes, which it could never do from zero. Big banks have already raised deposit rates to 0.3 percent, the highest since 1993. The only worry is that huge government loan, so the bank has to raise rates slowly and with care.

What India can learn

Now here is the interesting part. India is living the Japan story, but in the opposite direction and at high speed.

Japan had falling prices, India has steady rising prices. Japan had zero rates, India keeps rates clearly positive. And while Japanese families got stuck in cash, Indian families are now doing the very thing Japan wishes its own people would do. They are moving money out of plain savings and into investments. Bank deposits came down to about 35 percent of household savings, from 40 percent a year before. The money going into shares went up to about 15 percent from under 9 percent. Monthly SIP money has crossed 30,000 crore rupees, and for the first time the yearly SIP amount passed 3 lakh crore. A lot of this is coming from young people, women, and savers in smaller towns.

So what should India take from Japan?

First, use the young population while it is here. Japan grew old before it grew rich again. India still has many young workers, but this is a one time gift that will not last forever.

Second, do not fall into the gold trap. Japan held too much cash, India holds too much gold. Gold is fine in small amount, but locking huge money in a metal that makes nothing is the same mistake in a new shape. Better to keep putting money into things that grow and create jobs.

Third, respect the fear. A whole generation in India has only seen the market go up. Japan shows that markets can also fall hard and stay down for years. So treat a big fall as a sure thing one day, not a maybe, and build saving habits strong enough to survive that first crash.

A new chapter begins

For thirty years Japan showed the world what a flat market and zero interest do to people. They learn to fear shares and love cash. But here Japan's story is not completed.

Japan's story is still unfolding. After decades of near-zero interest rates, the Bank of Japan has started raising policy rates and allowing government bond yields to move higher. By June 2026, the policy rate had reached 1%, its highest level in more than 30 years.

This matters far beyond Japan. For years, Japanese investors searched for better returns overseas because yields at home were almost zero. As Japanese bond yields rise, some of that money could flow back into Japan, affecting global bond markets, stock markets, and currencies.