How RBI Controls Inflation: CRR, SLR, Repo and Reverse Repo

Most people have heard these terms in news but never really understood what they mean together. Let me try to explain it simply. First, Understand the Problem…

Most people have heard these terms in news but never really understood what they mean together. Let me try to explain it simply.

First, Understand the Problem RBI is Solving

Inflation means prices going up. When too much money is floating in the economy, people spend more, demand goes up, and prices rise. RBI's job is to control how much money is flowing in the system at any point.

RBI does not print money and hand it to people directly. It works through banks. Banks are the pipe through which money reaches to you and me. So if RBI wants to control money supply, it has to control what banks can do.

That is where CRR, SLR, Repo and Reverse Repo come in.

CRR: The Money Banks Cannot Touch

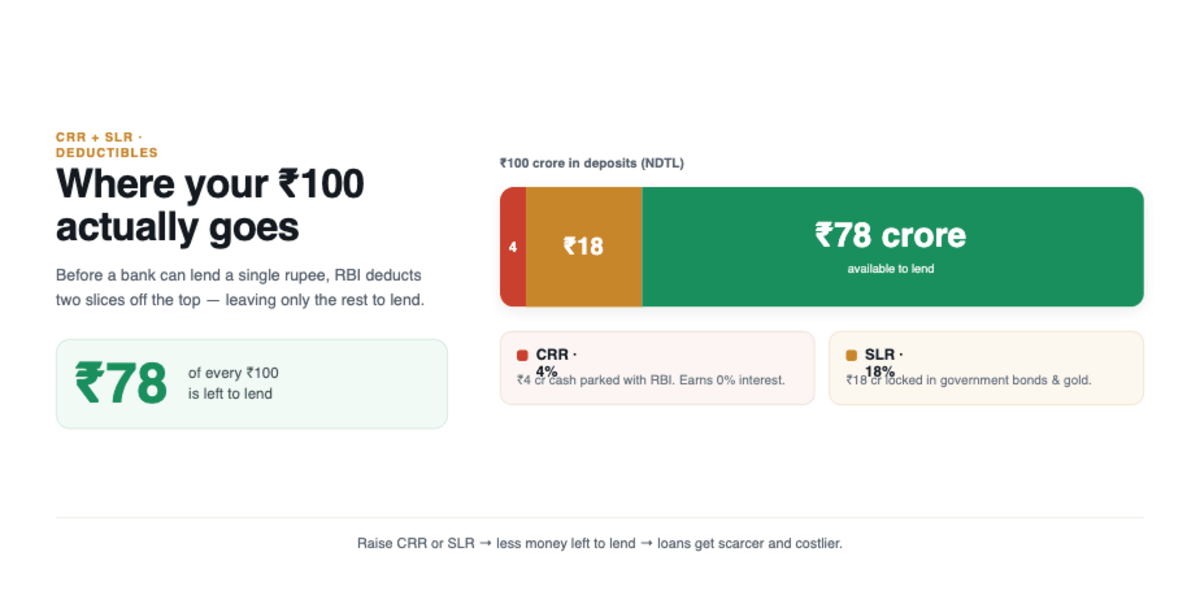

CRR stands for Cash Reserve Ratio. Every bank in India has to keep a certain percentage of its NDTL (Net Demand and Time Liabilities) with RBI. NDTL is basically all the money a bank owes to depositors and other banks, think of it as the bank's total liability pool not only just your saving account.

Banks cannot lend the CRR portion to anyone. It just sits with RBI. And here is the painful part for the banks because RBI pays 0% interest on it.

Example: If your bank has collected 100 crore in NDTL and CRR is 4%, the bank parks 4 crore with RBI and earns nothing on it. Only 96 crore can be lent out.

Now imagine RBI increases CRR to 5%. The bank can only lend 95 crore. And since that extra 1 crore is now earning 0.

This is why CRR is such a blunt and feared tool. It does not just reduce lending volume, it directly squeezes bank profits, which forces them to raise rates on you almost immediately.

SLR: The Money Banks Must Keep in Safe Assets

SLR stands for Statutory Liquidity Ratio. Apart from CRR, banks also have to keep another portion of their NDTL in safe government securities like government bonds.

Example: If SLR is 18%, the bank from our earlier example has to put 18 crore into government bonds or gold. Now out of 100 crore collected, only around 78 crore is actually available to lend after CRR and SLR both.

SLR also controls money supply, but it has a side benefit. It forces banks to buy government bonds, which helps the government raise money for its own spending.

Repo Rate: The Interest Rate Banks Pay to Borrow From RBI

Banks sometimes run short of cash. They can borrow money from RBI for short periods, usually overnight. The interest rate RBI charges for this is called the Repo Rate.

Example: If Repo Rate is 6.5%, a bank that borrows 100 crore from RBI overnight has to pay 6.5% annual interest for that period.

Now think about what happens when RBI raises the Repo Rate. Banks now have to pay more to borrow. So they charge more interest when they lend to you. Home loans, car loans, business loans all become expensive. People borrow less. They spend less and eventually Inflation cools down.

And, when RBI wants to boost the economy, it cuts the Repo Rate. Loans become cheaper. People borrow and spend more. Economy picks up.

Reverse Repo Rate and SDF:

What RBI Pays Banks for Parking Money

This is the opposite of Repo. When banks have excess cash and nothing to do with it, they can park it with RBI overnight and earn interest. That rate is called the Reverse Repo Rate.

But here is an important update. In April 2022, RBI quietly introduced something called the Standing Deposit Facility (SDF). It works exactly like Reverse Repo, where banks park excess money with RBI and earn interest. The difference is technical but significant: under Reverse Repo, RBI had to give government securities to banks as collateral. Under SDF no collateral is needed. RBI can absorb unlimited excess money from the system without that constraint.

Since April 2022, SDF has become the actual floor of the rate corridor, not the Reverse Repo Rate. The old fixed Reverse Repo Rate of 3.35% is now mostly dormant. As of mid-2026, with Repo at 5.25%, the SDF rate sits at 5.00%.

How These Four Work Together

Think of it like a tap and a bucket.

CRR and SLR decide how big the bucket is. How much of the deposited money actually becomes available for lending.

Repo Rate controls how easy or expensive it is to add more water into the bucket by borrowing from RBI.

Reverse Repo Rate controls whether banks want to give their water back to RBI instead of circulating it.

RBI uses all four together based on what the economy needs at that moment.

A Real Example: The Full Cycle from COVID to 2023

This is where everything clicks together. And it involves three phases, not one.

Phase 1: COVID hits (March 2020). RBI opens the tap fully.

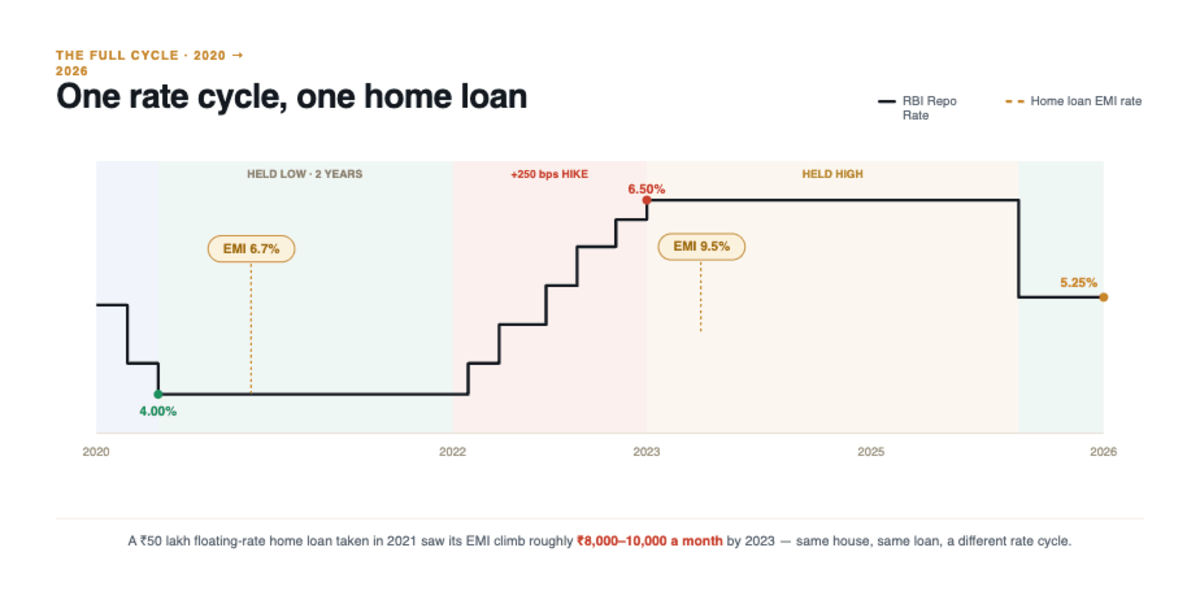

Economy was shutting down. Jobs were being lost. RBI's job shifted from controlling inflation to saving the economy. So it cut the Repo Rate from 5.15% to 4% in just two months i.e. in March and May 2020. It also cut CRR from 4% to 3%, pumping over Rs 1.37 lakh crore into the system. Banks had cheap money. They passed it on. By 2021, SBI and other banks were giving home loans at 6.7%, the lowest rate in decades.

If you bought a house in 2020 or 2021, you got a historic deal. That was RBI deliberately making money cheap to keep the economy alive.

Phase 2: RBI keeps rates low even through 2021 (the mistake everyone debates)

RBI kept the Repo Rate at 4% for two full years — May 2020 to April 2022. The thinking was that the economy was still recovering and it was too early to tighten. So cheap home loans continued well into early 2022.

Meanwhile, globally things were building up. Post-COVID, everyone started spending at the same time. Supply chains were still broken. Prices of goods started rising everywhere.

Phase 3: Russia invades Ukraine (February 2022). Everything breaks.

India imports over 80% of its oil. When Russia invaded Ukraine on February 24, 2022, Brent crude was already at $97 a barrel. Within two weeks it crossed $130, briefly touching $139 on March 7, the highest since 2008. That shock ran through everything like petrol, diesel, transport, food, manufacturing. Inflation in India went from 6% in January 2022 to 7.79% in April 2022 in just four months. RBI's acceptable ceiling is 6%. So 7.79% was a red alert.

On May 4, 2022, RBI hiked Repo Rate by 40 basis points to 4.4% and raised CRR by 50 basis points to 4.5%, draining Rs 87,000 crore from the system overnight.

Then it kept hiking every two months:

June 2022: 4.9% -> August: 5.4% -> September: 5.9% -> December: 6.25% -> February 2023: 6.5%

People who had taken floating rate home loans at 6.7% in 2021 were now paying close to 9.5% by 2023. Same loan, same house, EMI went up by Rs 8,000 to 10,000 per month. That is the real cost of a rate cycle turning.

By early 2023, inflation came back below 6%. RBI held rates at 6.5% for almost two years. Then, as growth slowed and inflation cooled, RBI started cutting. Through 2025 it cut three times, and by December 2025 the Repo Rate came down to 5.25%, where it stands today in mid-2026. Total reversal from the peak: 125 basis points cut so far.

So the person who had a floating rate home loan at 6.7% in 2021, saw it go to 9.5% by 2023, and is now watching it slowly come back down, that full cycle is the clearest real-world demonstration of how RBI uses these tools.

Why This Matters to You

If you have a home loan, the Repo Rate is probably already affecting your EMI. Most floating rate loans in India are now linked to an external benchmark, often the Repo Rate itself.

When RBI says it is cutting rates, your loan gets cheaper. When it hikes, your EMI goes up. Understanding why RBI is hiking or cutting helps you make better decisions. Are you taking a loan at the peak of the rate cycle? Should you wait? Should you prepay now before rates fall and your lender adjusts?

These are not just economic concepts. They directly touch your personal finance.

One Line Summary of Each Tool

CRR: Money banks must keep with RBI. Higher CRR means less money to lend.

SLR: Money banks must keep in government bonds. Controls lending and funds the government.

Repo Rate: Cost for banks to borrow from RBI. Higher rate means expensive loans for everyone.

Reverse Repo Rate / SDF: What RBI pays banks to park money. Since April 2022, SDF has replaced Reverse Repo as the active floor tool. Higher SDF rate pulls money out of circulation.

RBI moves these levers based on inflation data, GDP growth numbers and global signals. The goal is always the same: keep prices stable so the common person is not squeezed.

Sources:

Responses (0)

Leave a response

Related Articles

ULI vs OCEN: Why RBI Built a New Lending Platform When One Was Already There?

India has a interesting problem right now. We have not one but two digital systems trying to fix the same thing i.e. get…