ULI vs OCEN: Why RBI Built a New Lending Platform When One Was Already There?

India has a interesting problem right now. We have not one but two digital systems trying to fix the same thing i.e. getting loans to small businesses and…

India has a interesting problem right now. We have not one but two digital systems trying to fix the same thing i.e. getting loans to small businesses and people who banks usually ignore.

First came OCEN in 2020. Built by iSPIRT. Then in 2023, RBI announced their own thing, which is now called ULI, the Unified Lending Interface.

So the obvious question everyone should be asking is, if OCEN was already there, why RBI went and built ULI?

I have been thinking about this for a while, and the answer is more interesting than it looks.

They are not actually the same thing

On the surface both look similar. But the difference is in the philosophy, not the features.

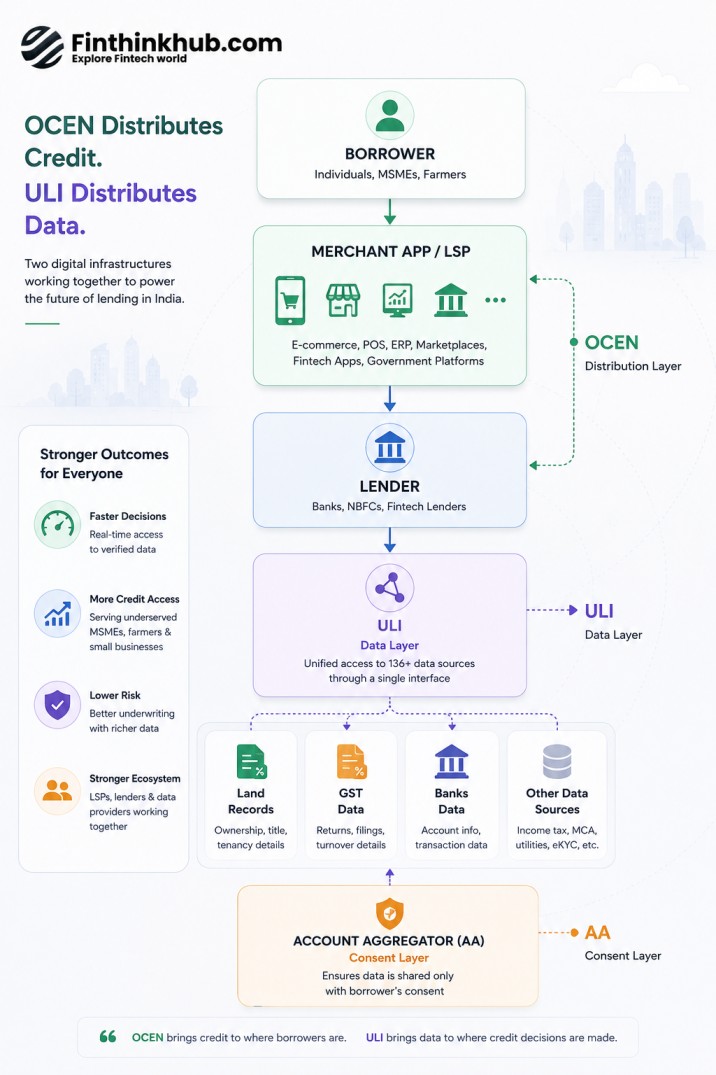

OCEN is a protocol. Think of it like a common language. Any app, be it ecommerce or a government marketplace, can use it to offer loans inside their own app. Nobody owns it, nobody runs it from the center. Fully market driven.

ULI is a platform. RBI's innovation hub runs it. It connects lenders to 100+ data sources like land records, GST filings, even milk supply data of dairy farmers. One thing to be clear though, ULI is not a lending app and it doesn't replace the lender's own underwriting or loan systems. It is the data pipe. The lending decision still sits with the bank.

OCEN ULI Made by iSPIRT (2020) RBI / RBIH (2023) Type Open protocol, no operator Central platform, RBI backed Main job Putting loans inside apps Giving lenders the data Numbers ~70,000 loans, ₹1,600 Cr in 2025 64 lenders, 12 loan journeys

So why did RBI launch ULI?

Could be, three reasons.

One, OCEN scaled, but only in a narrow lane. Five years have passed and OCEN's main success story is still GeM Sahay(Government EMarketplace). Yes the growth looks good on paper, disbursements grew 468% last year. But ₹1,600 crore in a country where total credit market is ₹170+ lakh crore? That is a rounding error. The protocol works, the ecosystem adoption didn't came at the speed anyone hoped. RBI saw the MSME credit gap was not closing and decided not to wait anymore.

Two, they solve different problems. OCEN fixes distribution, means how a borrower finds the loan. ULI fixes data, means what the lender knows about you. A dairy farmer's real problem is not finding a loan app. Her problem is no bank can check her land records and milk receipts without spending lot of time and money. ULI makes that one API call.

Three, and this is the big one, regulatory weight. When iSPIRT publishes a protocol, banks might adopt it. When RBI builds a platform, banks mostly will adopt it. Maybe not overnight, but the direction is set. ULI's lender count jumped from 36 to 64 in one year.

Okay, so who wins?

Case for ULI is strong. Regulator backing, lenders joining fast, and we have seen this movie before. UPI came with state backing and ate all the wallets. In India, the government anchored rail usually wins.

But the case for OCEN is also not dead. Protocols have a habit of outliving platforms. OCEN doesn't need to "win", it just needs to get absorbed. Its ideas around LSPs and embedded credit might quietly end up inside ULI's own design. And iSPIRT is already moving OCEN towards priority sector lending, a space where ULI is not playing.

There is also a middle path which I find most realistic. ULI becomes the data backbone, OCEN becomes the distribution layer carrying loans to apps where borrowers already spend their time. Plumbing and pipes. Not rivals.

The full stack, if you zoom out

Actually the cleanest way to see this is as three layers of India's lending stack, with Account Aggregator sitting quietly in the middle:

OCEN takes the loan to where the borrower already is. ULI fetches the verified data the lender needs. And Account Aggregator is the consent rail which makes sure that data moves only when the borrower says yes. Three different jobs. None of them replaces the other, and a loan in 2030 will probably touch all three without the borrower ever knowing their names.

What this means for you

If you are an NBFC or a fintech and can do only one integration, the lender migration is clearly telling where the center of gravity is. But if your whole business is embedded credit, lending inside someone else's app, then OCEN rails are still the only rails built for that. Uncomfortable truth of 2026 is, you probably need both.

The bigger lesson is about how India builds DPI itself. UPI worked because one body ran the rail and market competed on top. OCEN was an experiment. Can a pure protocol with no operator and no mandate do the same? ULI is RBI's answer so far, and the answer seems to be no. In lending, where trust runs much deeper than payments, India wants an anchor.

Is that the right answer or just the fastest one? That is the thing worth watching this year.

Sources: Medianama: ULI adds 64 lenders, 136 data services, RBIH: Unified Lending Interface, OCEN.dev, FrankBanker: Comparative look at OCEN and ULI, Medianama: iSPIRT PSLAI via OCEN

Responses (1)

- Rohan Singh28d ago

Amazing Article

Leave a response

Related Articles

How RBI Controls Inflation: CRR, SLR, Repo and Reverse Repo

Most people have heard these terms in news but never really understood what they mean together. Let me try to explain it…

Open Banking 2.0: When APIs Stop Sharing Data and Start Taking Action

India has always built financial infrastructure in layers. Aadhaar gave every citizen a verifiable digital identity. UPI…

How ML Models Are Replacing FICO/CIBIL Scores in Credit Underwriting

How ML Models Are Replacing FICO/CIBIL/Experian Scores in Credit UnderwritingCredit scoring has worked the same way for …