20-Year Journey: How Banking Technology Evolved from Legacy to API Ecosystems

Imagine it’s 2002. You walk into a bank branch and fill out a paper form, and wait in a queue. Your passbook gets updated manually or deposit cash. Fintech,…

Imagine it’s 2002. You walk into a bank branch and fill out a paper form, and wait in a queue. Your passbook gets updated manually or deposit cash.

Fintech, Mobile banking Unheard of ? Not even a buzzword !

Let’s understand the evolution of banking systems over the last 20 years — a journey from old legacy system to flexible API-based banking platforms powering today’s digital first banks.

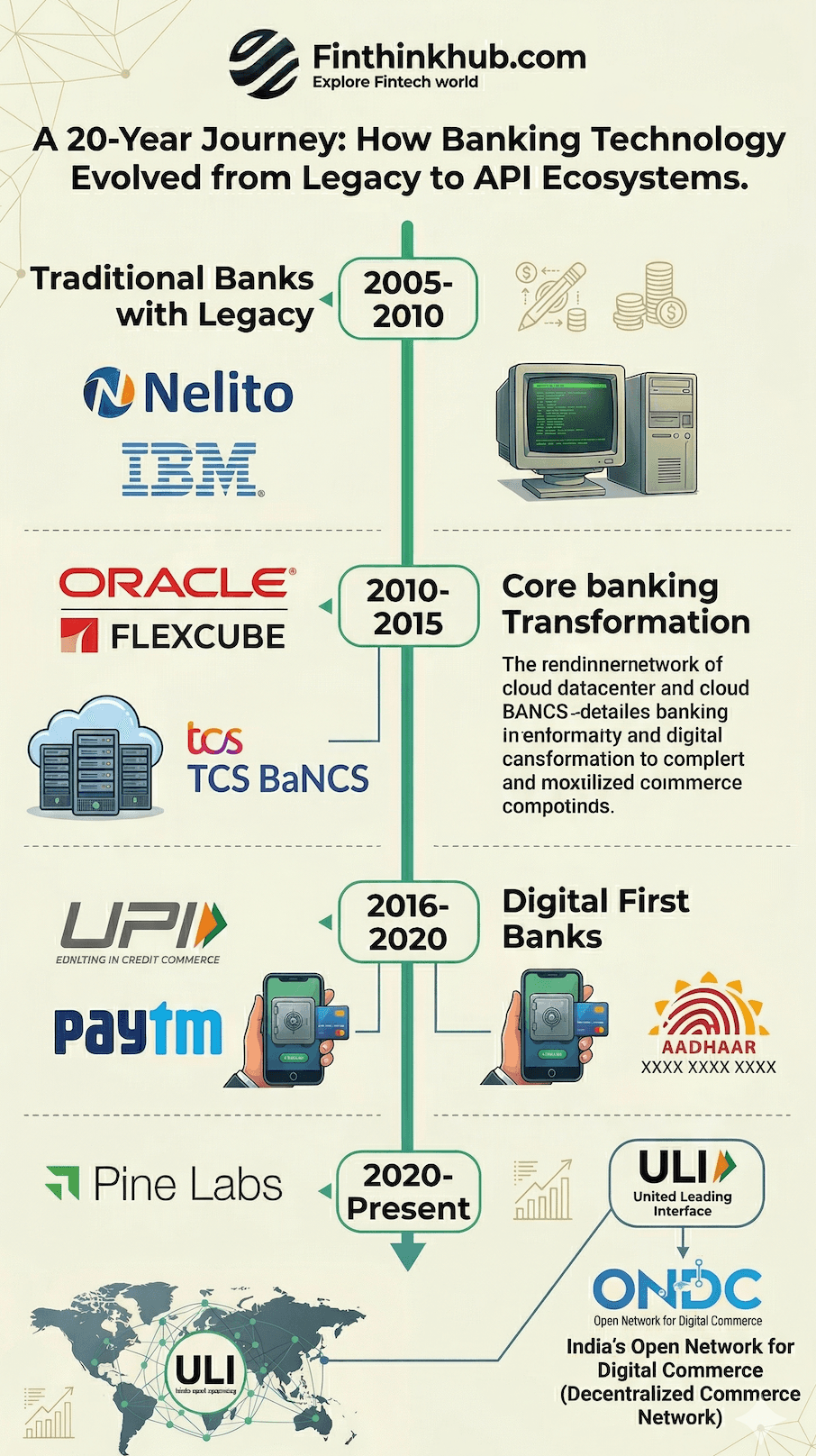

2005–2010: Legacy Systems & Fragmented Back Offices

In this period, banks were dependent on legacy mainframe systems. Many banks developed in-house system or sourced by early vendors. Some examples:

BIBAS (by Nelito) — Used by Rural Banks

BANCS24 — used by Bank of India

Banc 724 (by Zenith Software)

TBA (Total Branch Automation) Systems

MISR — legacy reporting system in many older banks

Tandem/HP NonStop — for transaction switches

AS/400-based systems — common in co-operative and regional banks

These systems were:

Batch-processed and offline in nature

Difficult to scale or integrate with third parties

Maintenance-heavy

Delay in transaction processing

Key Limitation: Branches were not fully connected, customers had to rely on the “home branch” for major transactions, sending money, cheque clearing process.

2010–2015: Core Banking Transformation Begins

As customer expectations increased, banks started migrating to modern Core Banking Systems (CBS). This was the first major digital transformation.

Popular Core Banking Platforms Introduced:

Finacle by Infosys — adopted by ICICI Bank, Union Bank of India, Bank of Baroda , majors PSU banks etc.

Flexcube by Oracle — used by HDFC Bank, Syndicate Bank, Canara Bank etc.

BaNCS by TCS — chosen by SBI for its massive transformation, Bank Of India etc.

Temenos T24 — Equitas Micro Finance India, And used in private and international banks

Benefits:

Centralized operations across all branches

Real-time transaction processing

Support for internet and mobile banking foundations

Banks could now offer basic online services, but innovation was still slow and internal.

2016–2020: Rise of Digital Banking Channels

As smartphones became widespread, digital banking exploded. Banks were started rolling out their mobile apps, web portals, digital lending and digital KYC on top of their CBS.

Key developments:

Launch of UPI, Aadhaar-based onboarding, and e-KYC

Banks began offering 24x7 banking with digital customer journeys

Shift to cloud-ready infrastructure

But banks still struggled to innovate fast. Why? Their core banking systems were monolithic, and digital experiences felt more like add-ons than a seamless part of the platform.

2020–Present: API Banking & Fintech Collaboration Take Center Stage

This period of true digital transformation, driven by:

Fintech revolution like Paytm, Phonepe, Digital Lending application like ziploan, Indifiloan etc.

Regulatory support (like Account Aggregators, RBI sandbox)

Open Banking & API Platforms launched: Banks built API platforms and have exposed their APIs service to the outerworld.

ICICI Bank — API portal

HDFC Bank — API Gateway

Yes Bank’s — YES Fintech Developer Portal

Axis Bank’s- Open APIs

Pine Labs , RazorpayX, Cashfree, Decentro building BaaS for fintechs

Banks exposed APIs for account info, fund transfers, mandates, UPI collections, and credit products.

Fintechs began embedding financial services:

NBFCs, Banks offering loans via Embedded Lending APIs

Insurtechs bundling insurance products for customer to provide products like Personal Insurance, Auto Insurance etc.

Wealth apps consuming mutual fund and demat APIs

Result:

Rapid innovation cycles

New revenue models via BaaS

Democratization of financial services

2023–Present: Banks as Platforms

Today, banks are evolving into platform providers or backend engine — offering financial rails to fintechs, merchants and other 3rd party entities.

Emerging themes:

Micro-services replacing monolithic cores

AI/ML for underwriting, fraud, and personalisation

Composable banking architecture

Real-time regulatory compliance and reporting

Ecosystem play with ONDC, OCEN, ULI and AA frameworks

Conclusion: From Banks to Banking-as-a-Service

In 15 years, banks have transformed from isolated legacy institutions into open, digital-first, API-powered ecosystems. The next phase will blur the lines even further — where customers may not even know who their bank is, but banking will be everywhere

Responses (0)

Leave a response

Related Articles

Neo-banks Have Great UX and Terrible Businesses. Here's Why.

They're beautiful. Onboarding in under 3 minutes. Spend analytics that your PSU bank will never build in your lifetime. …

The Core Components of the Banking as a Service Model (BaaS)

In a Banking as a Service (BaaS) model, multiple stakeholders play crucial roles, each with specific responsibilities. H…