Neo-banks Have Great UX and Terrible Businesses. Here's Why.

They're beautiful. Onboarding in under 3 minutes. Spend analytics that your PSU bank will never build in your lifetime. Zero forex markup. A support chat that…

They're beautiful. Onboarding in under 3 minutes. Spend analytics that your PSU bank will never build in your lifetime. Zero forex markup. A support chat that actually responds.

The UX is genuinely impressive.

And yet most of them are bleeding money. A few have pivoted to survive. One had to merge with a bank just to stay alive. The ones still standing are desperately trying to figure out how to turn a beautiful product into a business that makes sense.

This isn't a story about bad ideas. The people building Indian neo-banks are some of the sharpest operators in fintech. But there's a structural problem baked into the model that great design cannot fix.

Let me explain what I mean.

The Business of Banking Is the Balance Sheet. Neo-banks Don't Have One.

Here's the thing that's easy to miss when you're looking at a slick app: banking is fundamentally a balance sheet business.

Traditional banks make money on Interest Margin. They take your deposits at 3- 4% and lend it out at 10-12%. That 7-8% spread, applied across lakhs of crores of deposits is what funds everything: the branches, the staff, the bad loan provisions, and still leaves a profit.

Neo-banks don't have that.

Most Indian neo-banks aren't actually banks. They're either PPI licence holders, or they're a technology layer sitting on top of a partner bank (historically SBM Bank India, Federal Bank or RBL Bank have been popular choices for this). They don't hold deposits in any meaningful way. They don't lend on their own balance sheet.

Which means the entire Interest margin engine — the core of what makes banking profitable is completely absent.

Think about what's left: interchange on debit card transactions (which has been crushed), account maintenance fees (which nobody charges because it kills growth).

The revenue per active user for most Indian neo-banks is lower than the cost to acquirer them. The math doesn't work here.

Ref: The Jupiter FY24 data says that ("₹10 spent per ₹1 earned") from Inc42

UPI Killed the Last Revenue Line They Had

Timing matters here. Indian neo-banks launched into one of the most brutal monetisation environments in global fintech.

When UPI went zero-MDR in January 2020, it didn't just change payment economics. It eliminated the one easy revenue stream that neo-banks in the UK and US rely on "interchange" fees.

Monzo in the UK earns roughly £30–40 per active user annually just from Mastercard interchange when users spend on their debit card. N26 does something similar across Europe. That's a real, recurring revenue line.

In India, UPI is free. Debit card MDR is near-zero for most transactions. The government's vision for digital payments was to make them as frictionless as possible which is great for adoption and terrible for anyone trying to build a business on top of it.

Indian neo-banks are operating on the same playbook as their Western counterparts, in a market where the economics are structurally different.

I saw this up close at Paytm. Even at massive transaction scale — hundreds of millions of UPI transactions - the per transaction economics were brutal. The only way to make the numbers work was to push users up the value added service chain like into credit, into financial products, into BNPL and EMI. Pure transaction revenue was never going to be enough.

The CAC Trap

Let's talk about what it actually costs to acquire a neo-bank customer.

You need to spend on performance marketing. You need referral programmes (that ₹500 cashback for signing up your friend). You need influencer content, app store campaigns, and brand awareness. For a consumer fintech with no existing customer base, a fully-loaded CAC of ₹1,000-1,500 is not unusual.

And then what do you have?

A customer who opened an account for the free debit card and the ₹250 referral bonus. Who still uses HDFC for their salary account. Who uses the neo-bank for maybe 2-3 transactions a month — mostly for the nice UI or the forex rates when they're travelling.

The switching cost in Indian banking is very low for everyday transactions (because UPI is bank-agnostic) but very high for the things that actually generate revenue like salary accounts, home loans, FDs. So you get the wrong kind of sticky.

Retention is also harder than it looks. Neo-bank churn numbers are not publicly disclosed, but founders in the space will tell you that meaningful MAU-to-transacting user conversion is a constant battle. Beautiful app or not, people are lazy about changing their primary bank.

Slice's Moment of Honesty

The clearest signal that the standalone neo-bank model in India has limits came in 2023, when Slice merged with North East Small Finance Bank.

Slice had built a genuinely interesting product. A credit card for young, thin-file users. It had 10 million+ users, strong growth, and was one of the most-downloaded fintech apps in India.

And then they merged with a small finance bank.

Why? Because they needed a banking licence to do what they actually wanted to do — hold deposits, lend on their own balance sheet, and stop being entirely dependent on partner banks and NBFCs for the economics. The neo-bank layer was getting them users. It wasn't getting them a sustainable business.

The merger wasn't a failure. It was arguably the right strategic call. But it was also an acknowledgment that the pure neo-bank model, at least in India, runs into a wall without a licence.

Jupiter and Fi have both been quietly pivoting too. Jupiter launched mutual funds and stock investing. Fi pivoted hard into a "smart money app" — essentially becoming more of a financial management platform than a banking product. Every Indian neo-bank is looking for the same thing that a revenue line that isn't dependent on interchange or float.

What I'd Actually Watch For

I'm not writing this to say neo-banks are doomed. Some of them will survive and some will build genuinely good businesses.

But the ones that make it will look less like "banks with good UI" and more like financial platforms that happen to have banking features.

The interesting bets are the ones that use the customer relationship to distribute products they don't have to manufacture — mutual funds, insurance, credit cards via co-brand, loan referrals. Essentially, a brokerage model built on top of a banking interface. Revenue comes from distribution fees and not from the banking product itself.

The other path is the one Slice took that to get a licence, become a real bank, accept that you're in a heavily regulated, capital-intensive business, and build accordingly. Fewer startups can do this — but it's the only path to the full NIM engine.

What won't work is the current model at scale. Great UX got them users. They still need a business.

Responses (1)

- Yash30d ago

Nice article

Leave a response

Related Articles

Open Banking 2.0: When APIs Stop Sharing Data and Start Taking Action

India has always built financial infrastructure in layers. Aadhaar gave every citizen a verifiable digital identity. UPI…

The Core Components of the Banking as a Service Model (BaaS)

In a Banking as a Service (BaaS) model, multiple stakeholders play crucial roles, each with specific responsibilities. H…

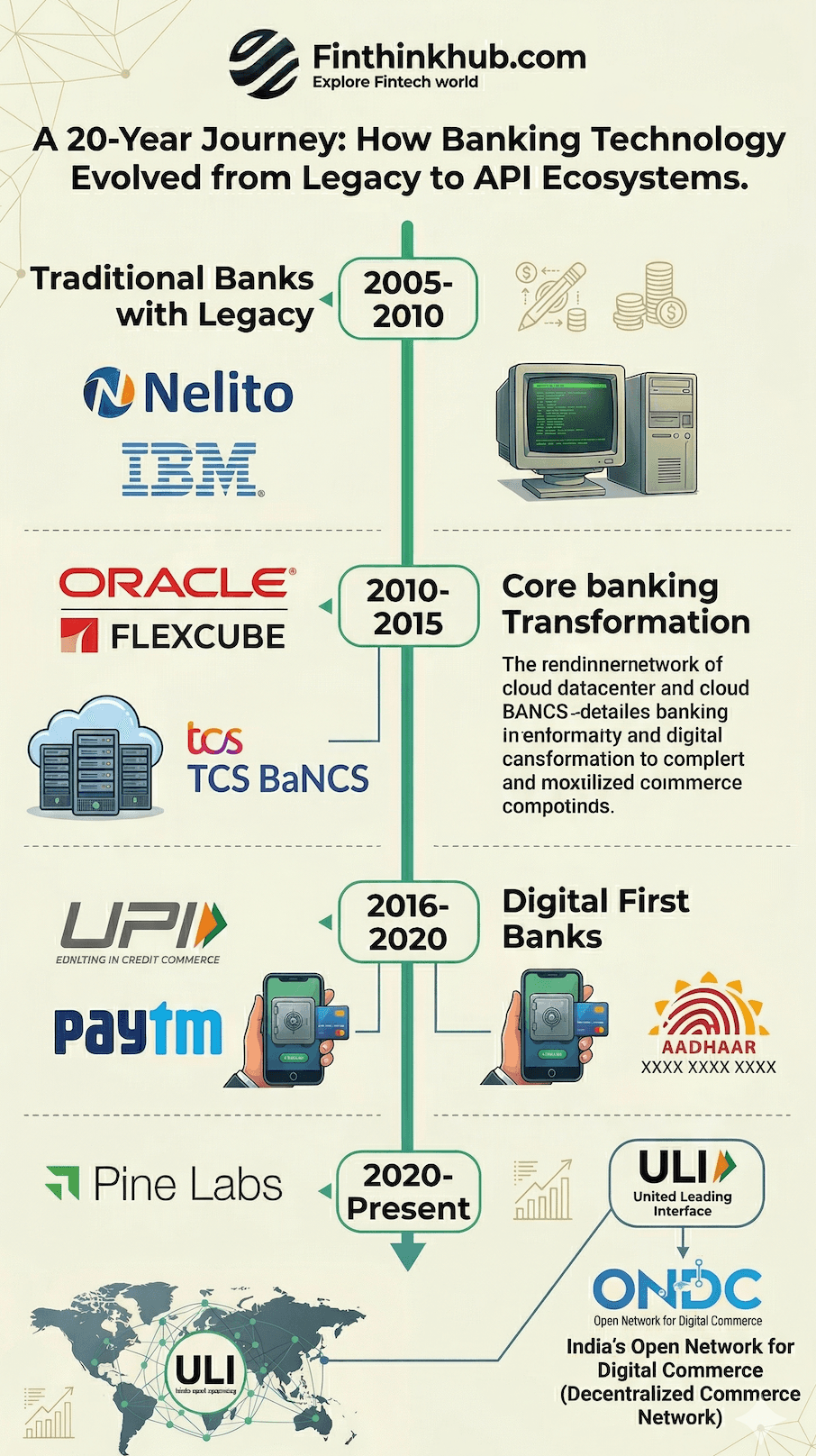

20-Year Journey: How Banking Technology Evolved from Legacy to API Ecosystems

Imagine it’s 2002. You walk into a bank branch and fill out a paper form, and wait in a queue. Your passbook gets update…